Written by Kha Nguyen

Edited by Genki Hase, Puspa & Chok

“Imagine you were a salaryman working for a Japanese company in Tokyo back in 1985, with stable income and abundant savings. Everything was on the rise, land and stock prices just went through the roof last year. If stock prices have fallen, who cares?

You’ll just buy some land and cover the losses. You decided to get bank loans to invest in real estate, with the intention of selling it high later on… 10 years later, your family is buried in debt.”

Interpreted from “Redoing Economic History – やりなおす経済史” (Kageyama, 2014).

This narrative represents only a fraction of the broader picture depicting Japan’s Lost Decade throughout the 1990s—a tumultuous decade characterized by economic stagnation, financial instability and social dislocation after the burst of the 1980s bubble economy. In the wake of the 2000s, Japan found itself grappling with the twin challenges of an aging population and heightened competition from China. These factors have impeded Japan’s efforts to rebound from recessions into a more robust and resilient growth path.

Yet, beyond the financial costs of the crisis, Japan was wounded with deeper, long-term scars: the brain drain of skilled workers and the loss of quality human capital within the industry. This reality was confirmed in a research conducted by Japan National Institute of Science and Technology Policy. From 1976 to 2015, more than 1,000 Japanese technical experts had left their home to join companies in emerging Asian competitors such as China, South Korea and Taiwan.

“Reverse brain drain”: the beginning of the end?

Timing, location, and harmony1 ― these are the foundational pillars of Japan’s remarkable economic success in the post-war era. With strong determination to revitalize the country and unmoving support from the United States, Japan emerged as a manufacturing hub during the Cold War era. Starting from scratch in 1945, it only took the country 20 years to become the second-largest economy in the world in 1968.

Since the 1950s, Japan has nurtured its core heavy industry, from automobile, shipbuilding, chemicals, steelmaking to electronics and semiconductor industry; all of which was substantially supported by the government throughout the research and development (R&D) processes. Many agencies, including the Ministry of International Trade and Industry of Japan, played a pivotal role in fostering growth of the electronics sector by streamlining access to funding for domestic corporations through established banking networks.

However, this export-oriented development was a double-edged sword for Japan. While this model spurred economic growth, it also made the economy increasingly vulnerable to external shocks such as fluctuations in global demand and the tariff impositions by key trading partners. Gradually, Japan’s economic miracle started to challenge the global dominance of the US, leading to trade friction over major export products like steel, automobile and semiconductor in the 1980s. This was inherently the perpetrator for the downfall of Japan.

In 1985, under the Plaza Accord, Japan was pressured to appreciate its currency against the dollar to “artificially”2 address the U.S. trade deficit. As the stronger yen made Japanese exports more expensive in foreign market, the country’s export-dependent economy began to suffer into a “high-yen”3 recession. In response, the Bank of Japan (BoJ) implemented a low interest rate policy to stimulate the economy, and Japanese firms began to invest their accumulated surplus capital from exports into real estate market. Little did they know, it was the ignition for the soaring asset price in land and stock.

The burst of the economic bubble was inevitable.

Nikkei Asia (2024). “On topic: What lies ahead for Japan after BOJ policy shift?”

U. Carmel (2017). “This is what a bubble looks like: Japan 1989 edition”. Standard & Poor’s; Japan Real Estate Institute

U. Carmel (2017). “This is what a bubble looks like: Japan 1989 edition”. Standard & Poor’s; Japan Real Estate Institute

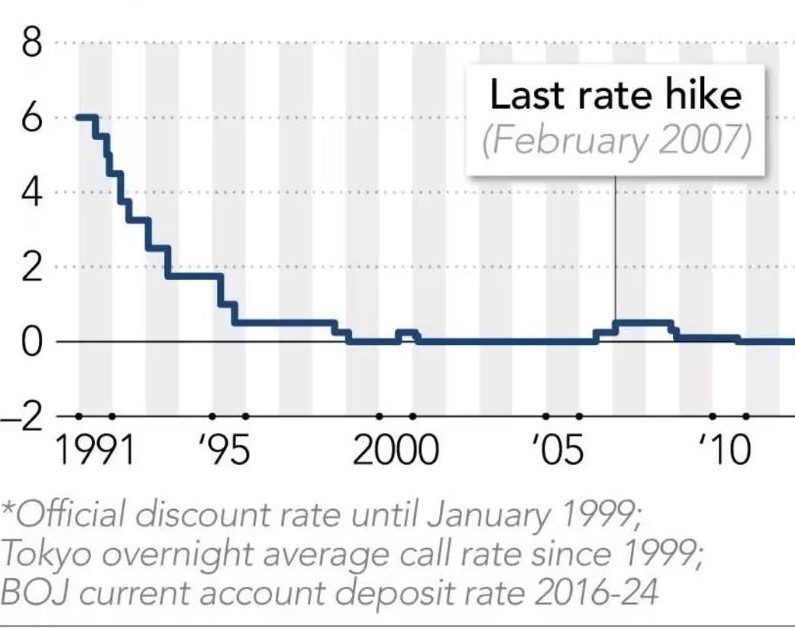

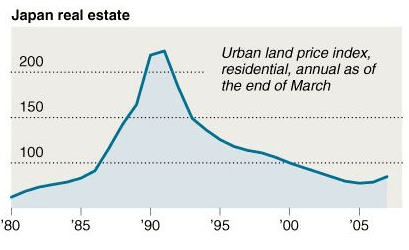

In order to cool down asset price inflation, the BoJ decided to raise the interest rates in 1990 (Figure 1), and this monetary tightening has accidentally triggered the collapse of stock and land prices. Stock market plummeted by more than 50% from its peak, while residential real estate prices tumbled by 20% prior to the crisis (Figure 2-1, 2-2). Confidence in domestic economy waned, big corporations and financial institutions drowned in debt, and growth in the manufacturing sector stagnated in spite of government’s rescuing efforts.

Due to an overwhelming number of bad loans originating from falling land prices, Japan’s banking system was squeezed to the brink of collapse with little capacity to provide lending to domestic firms. Big corporations were left struggling without sufficient resources to sustain their capital-intensive manufacturing businesses, while small and medium-sized enterprises starved for cash.

Together with substantial profits decline during the downturn, many firms resorted to downsizing their workforce and R&D activities while simultaneously shifting their production overseas to lower operational costs; all in the hope of staying competitive in the global market.

This strategy originally aimed for production cost reductions, yet it has two major consequences: facilitating the transfer of Japanese technology to neighboring countries like Korea and Taiwan, and creating a “reverse” brain drain4 for middle-aged professionals to move abroad for career advancement.

The case of Korea: the uphill battle

Korea was a latecomer in the race of electronics manufacturing, and the country’s entry into the industry during the 1970s followed four principles their Japanese rivals had practiced in the 1960s: mass production, foreign technology adoption, follow-the-leader strategy, and government support advantage.

The establishment of the Institute of Electronics Technology (KIET) during the 70s was part of the Korean government’s effort in building a cornerstone for semiconductor research. After opening a research center in the central Korean town of Gumi in 1976, KIET decided to set up joint ventures with VLSI Technology, a leading American semiconductor firm, to start a wafer fabrication capable of producing 16K-bit DRAMs (Dynamic Random Access Memory) by 1979. At that time, the first 16K RAM chip was the Intel 2116 introduced in 1976, and it was the state-of-the-art technology in the race of electronics between Japan and the US.

To bolster these initiatives, the Korean government also invited leading chaebols5—such as Daewoo, GoldStar, Hyundai and Samsung—along with their top talents, to contribute to this project with the aim of creating a hub for chip fabrication specialization. The objective was clear: to cultivate a thriving ecosystem of chip expertise within Korea.

Samsung was the pioneer for this project. With product lines consisting of TVs, radios, video cassette recorders (VCRs) and appliances, Samsung was uniquely motivated to develop its own DRAM technology. Despite getting rejected from Hitachi, Motorola, NEC, Texas Instruments, and Toshiba, Samsung finally secured Micron Technology as the only partner willing to license its 64Kb DRAM design in June 1983. Samsung went from zero to 64Kb DRAM fabrication in six months, with mass production kicking off in mid-1984.

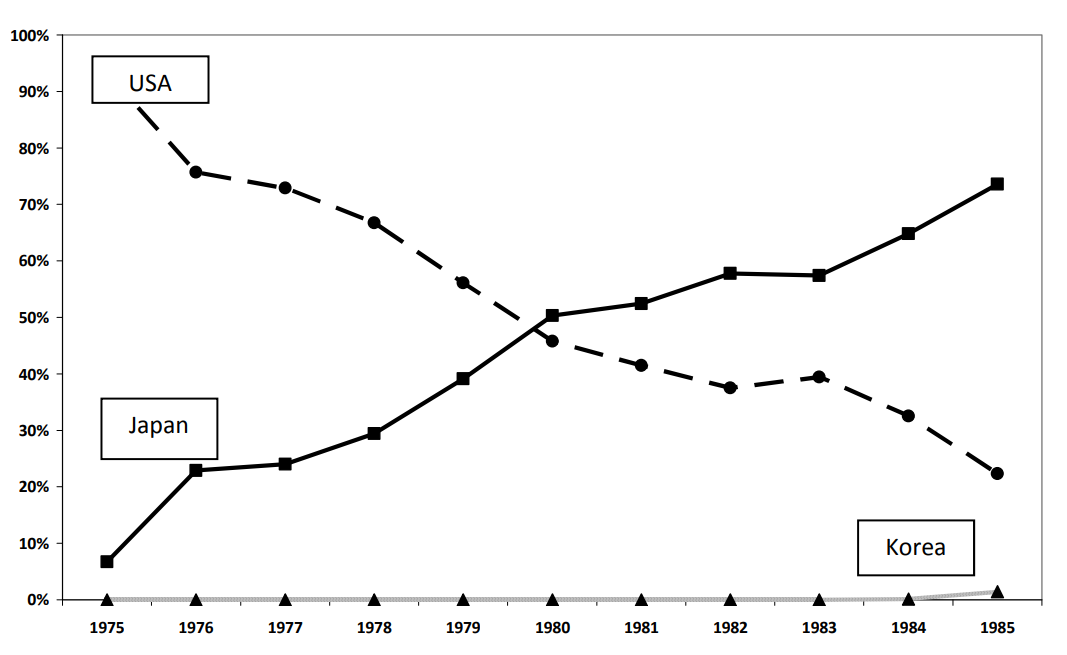

At that time, the DRAM market was fiercely competitive with constant development of higher-capacity chips in each new generation, and NEC, Hitachi & Fujitsu already all brought 64K DRAMs to the market five years ahead of Samsung in 1979. By the late 1980s, the world memory chip market was dominated by Japanese firms like Toshiba, Hitachi, Fujitsu and NEC, while US and European makers were crowded out (Figure 3). No one expected Korea would be a strong competitor to Japan.

Retrieved from Y. Shin (2015). “Dynamic Catch‐Up Strategy, Capability Expansion and Changing Windows of Opportunity in the Memory Industry”. GPN Working Paper

But, it all changed in the 1990s.

The collapse of Japan’s bubble economy in the early 90s has drained the financial resources of many Japanese electronics manufacturers, and the global recession in 1991 led to a drop in global demand. With dwindling profit margins and sales volumes, Japanese companies were coerced to implement drastic measures to reduce operational costs.

During the first two fiscal quarters of 1992, Pioneer Electronics, a leading global manufacturer of audio-visual equipment and car electronics business, wrestled with a staggering 44 percent drop in sales, and the company had to force 35 managers to leave before reaching their retirement age of 60. Likewise, employees at Matsushita Electric (now Panasonic Corporation), one of the world’s largest makers in consumer electronics in the 1980s, also found themselves pressured to either choose early retirement or relocation to a remote branch, where there is nothing to do but to stare at the keyboard. In that year, Japan’s Labor Ministry reported that over 300 companies had been laying off more than 30 workers each month—a twofold increase compared to the previous year’s figures during the same period.

Seizing this “recession” opportunity, Korean electronics giants like Samsung and LG moved swiftly to recruit Japanese engineers, who have strong expertise in materials, equipment, and methodology integral in Japanese technology. With mountains of fab investments exceeding $500 million annually over five consecutive years to transition to 200mm wafers6 production, Samsung surpassed Toshiba to become global DRAM market share leader in 1993 (Figure 4, 6). The company further invested in successive generations of DRAMs, and by 1995, Samsung achieved a significant breakthrough by being among the first companies to ship engineering samples of a 64-megabit DRAM. From then on, Korea started to outpace its Japanese counterparts in technological advancement. (Figure 5)

Retrieved from Y. Shin (2015)

Retrieved from Y. Shin (2015), Dataquest & iSuppli

Beyond the memory business, Korea also turned its attention to the flat panel display (FPD) industry in Japan. Back then among FPDs, the thin film transistor liquid crystal display (TFT-LCD) was the most promising and dominant technology due to its excellent image quality, consistent performance and cost-effectiveness. Recognizing this potential, Samsung had launched its own TFT-LCD divisions and initiated their intensive R&D efforts in TV technology in 1991. With the opening of their R&D Institute Japan in 1992, Samsung wasted no time in recruiting numerous Japanese experts, leveraging the surplus of skilled human resources made available by the first decline of Japan’s FPD industry in 1993-94. Substantial R&D and investment laid the groundwork for their next major move, as Koreans awaited for the next downturn to launch a full-scale offensive (Matthew, 2005). Samsung inaugurated its first domestic TFT-LCD mass production line in March 1995, with the subsequent launch of their second and third LCD lines in 1996 and 1998, respectively.

However, nothing was guaranteed; when the Asian financial crisis struck Korea in 1997, Samsung was deep in debt and approaching bankruptcy. To recover, the company took immediate action―reducing 30% of its workforce and enforcing significant cuts in assets as well as unprofitable businesses within just 18 months. While restructuring, Samsung took risks on memory technology.

Jong Yong Yun, former vice chairman and CEO at Samsung Electronics, observed the global industry and saw the Japanese no longer investing, while Micron in the US and Siemens in Europe weren’t doing well either. As the world got skeptical of the cyclical nature of the memory business, it was when Samsung took a move and continued their investment in chip manufacturing facilities (Figure 6)

Shin & Jang (2005). “Creating First-Mover Advantages: The Case of Samsung Electronics”. SCAPE

“The memory business is all about scale,” said Nam Hyung Kim, director and chief analyst at market research firm iSuppli. Cost control is everything; and most suppliers need to operate “mega-fabs” with a monthly output of at least 150k to 200k wafer to leverage economies of scale and drive down costs.

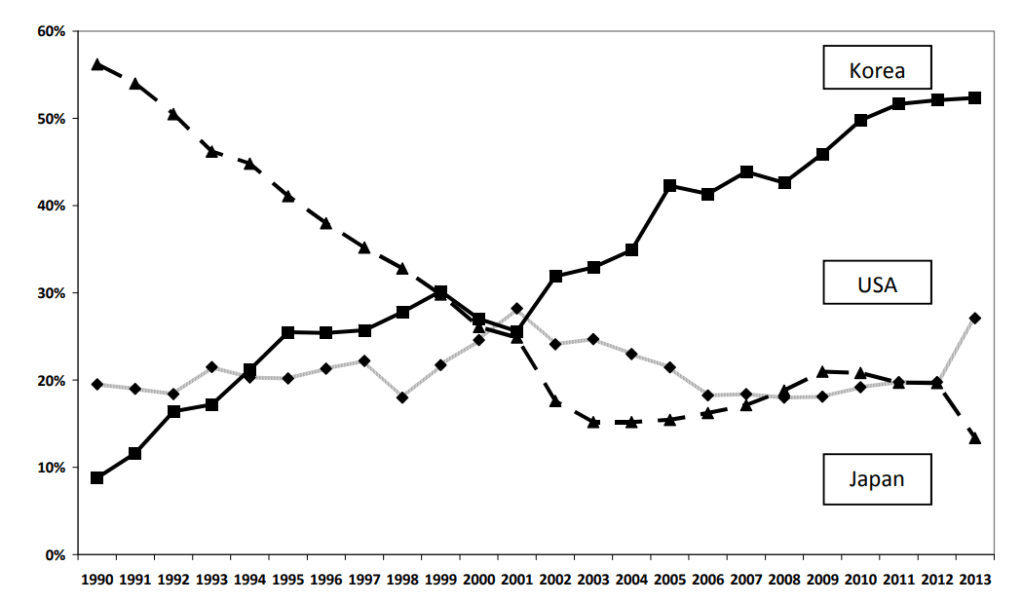

In terms of display panel market, although both Japanese and Korean companies were in distress from the economic downturn, Korean TFT-LCD manufacturers adopted a competitive low-price strategy and drastically expanded their global market share amid the depreciating value of the Korean won. Between 1997 to 1998, the share of Korean manufacturers in the global FPD market doubled from 15% to 30% (Figure 7), posing major threats to the longstanding dominance of Japanese electronics giants in the TV industry.

Retrieved from K. Asakawa (2007). “Metanational Learning in TFT-LCD Industry”. RIETI

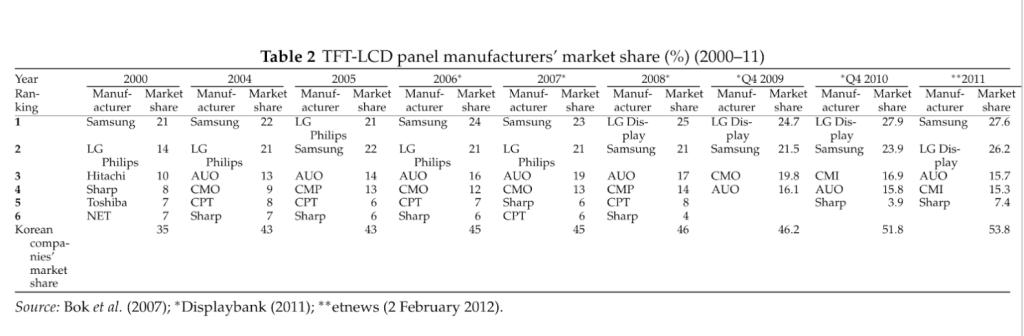

Until 1995, Japanese consumer electronics giants controlled over 80% of the global LCD supply, with their dominance extending to over 90% of the TFT-LCD market. However, by the 2000s, Samsung and LG had risen to the top two spots in global market share, eclipsing the former leading of Japanese electronics firms (Table 2). As Japanese companies faced declining market share alongside prolonged banking crises and the dot-com recession in late 1990s, they entered into vicious cycles of losses and downsizing.

Retrieved from YS. Lee (2013). “The state role as an inter-scalar mediator in globalizing LCD industry development in Korea”. Review of International Political Economy

Toshiba Corp, Japan’s largest chipmaker, announced plans to slash 18,800 domestic jobs in 2001 as it faced its worst net loss ever. With an unprecedented net loss of 123.1 billion yen ($1 billion) for the first half of the business year, the company also revealed intentions to close six out of its 21 domestic plants by year-end, part of a strategic move to shift manufacturing operations overseas to reduce costs. NEC, Japan’s second-largest chipmaker only behind Toshiba, also posted a net loss of 155.0 billion yen ($1.17 billion) for Q3 2001, resulting in 14,000 jobs cut running for corporate restructuring through March 2002.

In such a bleak economic landscape and waves of layoff, an enormous, yet invisible outflow of Japanese workers to overseas companies in search of fresh new opportunities started to boom. While some had no choice but to move abroad after being forced into early retirement, others chose to pursue their career overseas where R&D opportunities were much more performance-based and self-determined.

In his autobiography “The Secrets of Korean Elites: What I learned from Working at Samsung”7, Takahisa Mizuta, an engineer with over a decade of experience at Hitachi in the 1990s, reflects on his career journey before joining Samsung Group in 2000. During his time at Hitachi, Mizuta played a crucial role in developing key components for cathode ray tube (CRTs) in televisions. Although he proposed a study on the computerized test manufacturing of parts, it was rejected by his supervisors who argued that it was not a manufacturing technology. It took years before Mizuta was granted permission to conduct the research, only to be subsequently transferred to the large-size plasma display panels department.

A senior colleague at Hitachi, who had transitioned to Samsung, encouraged him to move abroad for personal professional growth: “You will find other opportunities here (in Seoul). At Samsung, you can utilize your skills to develop components”

As a new-comer, Samsung lacked technical capabilities to produce core parts for their CRTs. When Japanese firms such as Hitachi and Panasonic began to shut down their tube TV production line in the early 2000s, Korean companies were trying to search for Japanese engineers involved in CRTs production to re-develop this abandoned technology.

Mizuta quickly received an employment contract at Samsung R&D Institute Japan in Yokohama just 2 months after his “senpai” at Samsung recommended him. In South Korea, Mizuta enjoyed the freedom of discovery, which was a rewarding experience for him as a researcher.

Fukugawa Hiroshi, a professor of Asian study in Kyushu University, has illustrated the deliberate pattern of Japanese tech brain drain migrating to Korea through his interview with Mr. B, a retired expert in TV display technology. “Mr. B acknowledged that the decline of display technology in Japanese companies forced him to change his career to Korea, where his expertise remained applicable.”

Another Japanese engineer, a man in his 50s working at Ricoh Corp, received a job offer last summer from a Korean firm after being suddenly pushed into early retirement due to his company’s declining profits. Once again, the recruitment email came from Samsung R&D Institute Japan, as Samsung was seeking specialists in laser-based copying technology, particularly those with experience in copy machine development at companies like Ricoh, Fuji Xerox, Canon, or Konica Minolta that Korean giants desperately needed. Surprisingly, he wasn’t the first Japanese expert in this field: during the interview at the institute, one of the three interviewers was a Japanese engineer who had previously worked for a Japanese manufacturer.

It was the year of 2013, and Samsung has been approaching him for more than 10 years.

The case of Taiwan: Follow the flow

During the 1980s, Taiwan was still in its infancy stage of the electronics industry. Inspired by the Silicon Valley technology hub in the US, Taiwan’s Minister of Science and Technology has established Hsinchu Science Park to foster the innovation of scientific and technological frontiers, where Taiwanese entrepreneurs could integrate the technology learned in the US to lay the cornerstone of Taiwan’s semiconductor industry. It was the birthplace of Taiwan Semiconductor Manufacturing Company (TSMC), the current world’s largest chip maker by revenue.

In the 1990s, amidst the spiraling competition with Korea in the semiconductor industry and higher domestic production costs, Japanese electronics giants began to collaborate with Taiwanese firms to avoid being “caught up” with their Korean counterparts. Exhausted in the race of memory chips, it was the TFT-LCD industry that sparked the technology transfer and the mobility of human resources from Japan to Taiwan.

TFT-LCD8 is a technology-intensive industry that requires about US$700 million in equipment investment per plant. Technology innovation in the TFT-LCD industry is extremely rapid; therefore, manufacturers have to raise funds from the capital market continuously to invest into production and R&D capabilities. However, due to the financial crisis in the late 1990s, Japanese firms were falling into cycles of debt and corporate restructuring, restricting their ability to invest in new equipment. Since then, Japan’s LCD industry has faced challenges of keeping pace with its Korean competitors.

In a bid to rival chaebols, Japanese firms have pursued various initiatives, including technology licensing agreements and collaborative ventures with Taiwanese manufacturers.

In 1997, Chunghwa Picture Tubes (CPT) was the first manufacturer in Taiwan to successfully introduce large-scale TFT-LCD technology from Mitsubishi ADI. In 1998, Acer Display Technology introduced 3.5 generation TFT-LCD technology from IBM Japan, and later adopted Multi-domain Vertical Alignment (MVA) technology from Fujitsu, marking a breakthrough in large-scale TFT-LCD production in 2000. Unipac Optoelectronics and HannStar Display were also among the beneficiaries of know-how diffusion from Panasonic and Toshiba with many technology transfer contracts. (Wang, 2003)

Professor Mayumi Tabata, a Japanese economic sociologist on Japan-Taiwan industrial development mechanism, found out that while benefiting from the technology transfer, Taiwanese firms have also actively employed Japanese talents to fulfill their hunger for expertises in the high-tech industry. For instance, Quanta Display has historically recruited senior technicians from Mitsubishi Electric Corporation, many of whom had previously worked at Quanta Display R&D center in Japan. Similarly, Prime View International, the first TFT-LCD manufacturer in Taiwan, has also appointed experienced Japanese executives to key positions.

This success was not a pure miracle. In 1987, the Industrial Technology Research Institute (ITRI) partnered with Taiwan’s Ministry of Economic Affairs to establish their satellite office in Tokyo, aimed at facilitating the recruitment of Japanese technical personnel and executives for local TFT-LCD firms.

Retrieved from M. Tabata (2012). “The Absorption of Japanese Engineers into Taiwan’s TFT-LCD Industry”. Asian Survey, University of California Press

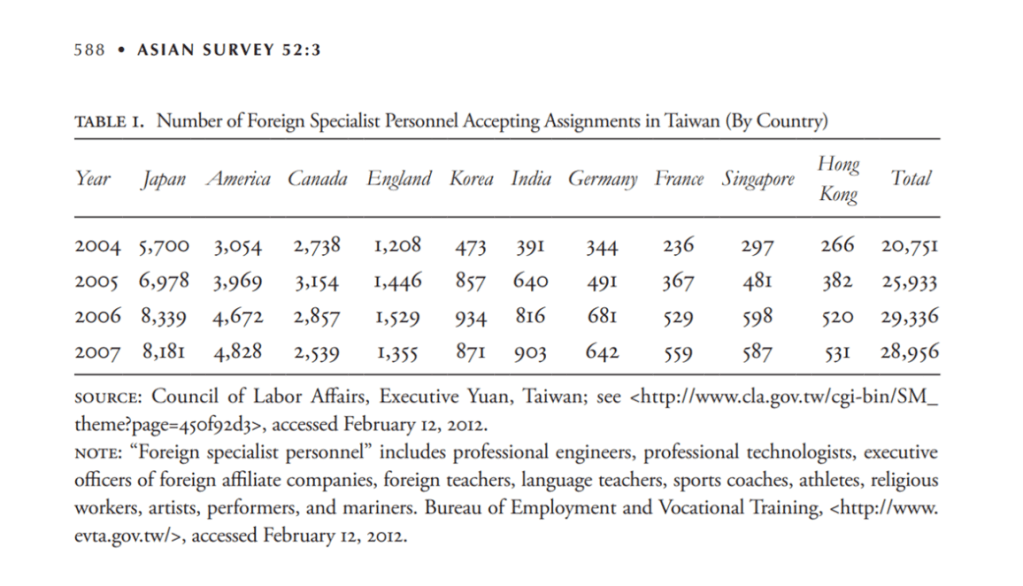

According to Taiwan’s Council on Economic Planning and Development (CEPD), the number of Japanese specialist personnel obtaining work permits in Taiwan surged from 5,700 in 2004 to over 8,000 by 2007 (Table 1). However, despite this technology collaboration initially aiding Japanese firms in their short-term survival, they didn’t anticipate the transformation of their Taiwanese allies into rivalry. (Tabata, 2012)

To protect the technology, Sharp filed for a court injunction to halt sales of LCD televisions manufactured by Taiwan’s Teco Electric and Machinery Corp. Group, claiming the firm was violating its patents in 2004. But it was all too late.

Since 2002, Hitachi, Toshiba, NEC and Mitsubishi Electric (excepting Sharp) have gradually scaled down their operation in the large-size TFT-LCD business in contrast to the rise of Korean and Taiwanese tigers (Table 2). With the disappearance of TFT-LCD businesses in Japan, Japanese talents started to drain out: many experienced Japanese engineers from major Japanese electronics companies had no choice but to work in Taiwanese firms, including the upstream chip memory industry.

Heiji Kobayashi, a 41-year-old semiconductor engineer, faced a dead-end career when Mitsubishi Electric withdrew its chip business in the early 2000s. Kobayashi then moved to Taiwan’s booming chip industry, where he found his new role at Powerchip Semiconductor as deputy director overseeing factory production line design.

“In Asia, we can keep contributing to society,” said Katsumitsu Nakamura, another former Hitachi engineer who came to Taiwan. “In Japan, we would just be collecting pensions.”

Similarly in 2005, 51 year old Tatsuo Okamotomade made a bold move by leaving his position as an engineer at Renesas Technology to work at Winbond Electronics in Taiwan. For him, joining Taiwanese firms was a “high-risk, high-return decision.”, while staying in Japan has become “high risk, low return”

According to the NY Times, Kobayashi, Nakamura, and Okamoto are just three examples of thousands of Japanese engineers, who left their jobs in Japan in pursuit of opportunities in Taiwan.

Over the last three decades, Taiwanese and Korean firms have taken advantage of Japan’s recession since the 1990s to entice high-skilled Japanese engineers with their tacit knowledge in technological know-how in the global race for semiconductor supremacy. They internalized core technology, transformed it into standardized production with experienced workforces, and fostered innovation to create their next-generation high-tech industry accompanied by the side-by-side government assistance.

The brain drain of Japanese technical experts highlights the convergence of Japan’s economic crisis, stagnated corporate structures, and the rise of Asian superpowers. Seemingly resting in their “economic miracle” laurels, Japan had fallen behind in crucial technology progress, such as smartphone revolutions in the era of digitalization. It wasn’t until 2005 that Japan set up its first Semiconductor Technology Academic Research Centre for industry-academia collaboration, whereas the United States had already pioneered such initiatives with the Semiconductor Research Corporation since 20 years earlier back in 1982, Taiwan’s Industrial Technology Research Institute (ITRI) in 1973, and Korea’s Electronics and Telecommunications Research Institute (ETRI) in 1976.

Surely, Japanese electronics giants will rebound with the increasing demand for high-end chips driven by the rise of AI. But history remained valuable lessons for Japan’s next big leap.

Indeed, what’s the cost of the Lost Decade to Japan?

It’s a lost generation.

Reference

Kang, Sato & Ueki, 2017. “Mobility of Highly Skilled Retirees from Japan to the Republic of Korea and Taiwan”, ERIA Discussion Paper Series

https://www.eria.org/publications/mobility-of-highly-skilled-retirees-from-japan-to-the-republic-of-korea-and-taiwan

Kazuhiro Asakawa, 2007. “Metanational Learning in TFT-LCD Industry: An Organizing Framework”, RIETI Discussion Paper Series 07-E-029

https://www.rieti.go.jp/en/publications/summary/07050003.html

Hiroshi Fukagawa, 2012. “A study on the Role of Japanese Engineers in Korean Industrial Innovation”, The Journal of Korean Economic Studies

https://doi.org/10.15017/4738310

Mayumi Tabata, 2012. “The Absorption of Japanese Engineers into Taiwan’s TFT-LCD Industry”, Asian Survey, vol. 52 (no. 3), pp. 571-594, University of California Press

https://doi.org/10.1525/as.2012.52.3.571

Mayumi Tabata, 2014. “The rise of Taiwan in the TFT-LCD industry”, Journal of Technology Management in China, vol. 9, no. 2, pp. 190-205

https://doi.org/10.1108/JTMC-12-2013-0040

Ikeda, Hosokawa, 2017. “Japan seeks to stop tech brain drain”, Nikkei Asia

https://asia.nikkei.com/Business/Japan-seeks-to-stop-tech-brain-drain

Kyodo, 2003. “Matsushita to halt CRT production”, The Japan Times

https://www.japantimes.co.jp/news/2003/11/09/national/matsushita-to-halt-crt-production/

P. Alpeyev, T. Culpan, 2010. “Hitachi, Hon Hai in Talks on LCD Business Cooperation”, Bloomberg

https://www.bloomberg.com/news/articles/2010-12-28/hitachi-says-it-s-in-discussions-with-hon-hai-on-lcd-business-cooperation

Industry Analyst Inc. 2013. “Japanese Engineers in Demand in South Korea and China” “Japanese Engineers in Demand in South Korea and China”

https://www.industryanalysts.com/japanese-engineers-in-demand-in-south-korea-and-china/

CNN, 2001. “Toshiba slashes outlook after $1B loss in 1H”

https://edition.cnn.com/2001/BUSINESS/asia/10/26/toshiba.earnings/index

Miki Tanikawa, 2001. “Toshiba to Cut 19000 Jobs Amid Japan Technology Slump”, The New York Times

https://www.nytimes.com/2001/08/28/business/toshiba-to-cut-19000-jobs-amid-japan-technology-slump

CNN, 2002. “NEC warns on profits, cuts jobs”

https://edition.cnn.com/2002/BUSINESS/asia/01/31/japan.nec/index.html

Chicago Tribune, 2001. “Fujitsu to cut 16,400 jobs as chips slump”

https://www.chicagotribune.com/2001/08/21/fujitsu-to-cut-16400-jobs-as-chips-slump/

Forbes, 2002. “Unsung hero”

https://www.forbes.com/global/2002/0624/030.html?sh=e0c00853da30

YS Lee, I. Heo & H. Kim, 2013 “The role of the state as an inter-scalar mediator in globalizing liquid crystal display industry development in South Korea”, Review of International Political Economy, vol. 21, pp. 102-129

https://doi.org/10.1080/09692290.2013.809781

TY Park, JY Choung, HG Min, 2008. “The Cross-industry Spillover of Technological Capability: Korea’s DRAM and TFT–LCD Industries”, World Development, vol. 36, no. 12, pp. 2855-2873

https://doi.org/10.1016/j.worlddev.2007.11.005

Y. Kim, 1998. “Technological capabilities and Samsung Electronics’ international production network in East Asia”, Management Decision, vol. 36, no. 8, pp. 517-527.

https://doi.org/10.1108/00251749810232592

Kim Chang-Wook, Hyundai Research Institute, 1999. “Semiconductor Industry of Korea”

https://www.hri.co.kr/upload/board/EVP199503_06.PDF

Andrew Pollack, 1982. “Japan’s big lead in memory chips”, The New York Times

https://www.nytimes.com/1982/02/28/business/japan-s-big-lead-in-memory-chips.html

The New York Times, 1997. “Samsung Cuts Jobs and Pay As Koreans Brace for Pain”

https://www.nytimes.com/1997/11/27/business/international-business-samsung-cuts-jobs-and-pay-as-koreans-brace-for-pain

Tampa Bay Times, 1993. “Even in Japan, some companies can’t avoid layoffs in recession”

https://www.tampabay.com/archive/1993/01/10/even-in-japan-some-companies-can-t-avoid-layoffs-in-recession

Richard J. Schmidt, 1997. “Japanese management, recession style”, Business Horizons (vol. 39, issue 2)

https://doi.org/10.1016/S0007-6813(96)90025-7

David E. Sanger, 1993. “Layoffs and Factory Closings Shaking the Japanese Psyche”, The New York Times

https://www.nytimes.com/1993/03/03/business/layoffs-and-factory-closings-shaking-the-japanese-psyche.html

EE Times, 2008. “How Samsung out-hustled Japan Inc.”

https://www.eetimes.com/how-samsung-out-hustled-japan-inc/

Chico Harlan, 2012. “As Apple and Samsung dominate, Japan’s tech giants are in a free fall”, The Washington Post

https://www.washingtonpost.com/world/as-apple-and-samsung-dominate-japans-tech-giants-are-in-a-free-fall/

Charlie Campbell, 2021. “Inside the Taiwan Firm That Makes the World’s Tech Run”, TIME

https://time.com/6102879/semiconductor-chip-shortage-tsmc/

The Japan Times, 2004. “Sharp moves to block Taiwan rival’s sales of LCD televisions”

https://www.japantimes.co.jp/news/2004/06/11/business/sharp-moves-to-block-taiwan-rivals-sales-of-lcd-televisions/

Martin Fackler, 2007. “A Japanese Export: Talent”, The New York Times

https://www.nytimes.com/2007/05/24/business/worldbusiness/24braindrain.html

Taipei Times, 2007. “Taiwan wooing Japanese talent”

https://www.taipeitimes.com/News/biz/archives/2007/05/25/2003362422

Jon Y, 2023. “The 20 Year Fall of Japan’s Sharp Corporation”, The Asianometry Newsletter

https://www.asianometry.com/p/the-20-year-fall-of-japans-sharp

Jon. Y (2023). “The Rise and Peak of Japanese Semiconductors”. The Asianometry Newsletter

https://www.asianometry.com/p/the-rise-and-peak-of-japanese-semiconductors

TW Lei, 2023. “Japanese Semiconductor Industry’s Collaboration with Taiwan Semiconductor Manufacturing Company”, East Asian Policy, vol. 15, no. 01, pp. 47-59

https://doi.org/10.1142/S1793930523000041

H. Bauer, S. Burghardt, S. Tandon, F. Thalmayr, 2016. “Memory: Are challenges ahead?”, McKinsey & Company

https://www.mckinsey.com/industries/semiconductors/our-insights/memory-are-challenges-ahead

Semiconductor History Museum of Japan, Society of Semiconductor Industry Specialists

https://www.shmj.or.jp/english/trends/trd90s.html

Wang, 2003. “The secret of Taiwan to the LCD Kingdom” (Chinese: “台湾邁行液晶王国之秘”)

Daniel Nenni, 2019. “A Detailed History of Samsung Semiconductor”, SemiWiki

https://semiwiki.com/semiconductor-manufacturers/samsung-foundry/7994-a-detailed-history-of-samsung-semiconductor/

U.S. Congress, Office of Technology Assessment, 1995. “Flat Panel Displays in Perspective”, OTA-ITC-631

https://apps.dtic.mil/sti/citations/tr/ADA337367

IMF (2009). “Revisiting Japan’s Lost Decade” https://www.elibrary.imf.org/display/book/9781589068407/ch04.xml

Fei Han (2019). “Demographics and the Natural Rate of Interest in Japan”. IMF

https://www.elibrary.imf.org/view/journals/001/2019/031/article-A001-en.xml

Kageyama (2014). “Redoing Economic History” (Japanese: “やりなおす経済史”) https://booklive.jp/product/index/title_id/286420/vol_no/001

Shiraishi, M. (1990). “Japan’s Relations with Vietnam 1951 – 1987”. Cornell University.

https://www.cornellpress.cornell.edu/book/9780877271222/japanese-relations-with-vietnam-19511987/#bookTabs=1

Havens Thomas, R.H. (1987). “Fire Across the Sea – The Vietnam War and Japan 1965 –1975”. Princeton University Press

https://press.princeton.edu/books/hardcover/9780691638058/fire-across-the-sea?srsltid=AfmBOop4WedoH8-bQ6tslC8q08sD3v5Mv1nyVMN18coZ7BA-6ne7Jpwm

Schaller, M. (1997). “Altered States”. Oxford University Press.

https://ci.nii.ac.jp/ncid/BA33106816#anc-library

Ishimaru Yasuzo (2007). “The Korean War and Japanese Ports: Support for the UN Forces and Its Influence”. NIDS Security Reports

https://www.nids.mod.go.jp/english/publication/kiyo/pdf/2007/bulletin_e2007_5.pdf

Shinji Yoshioka & Hirofumi Kawasaki (2016). “Japan’s High-Growth Postwar Period: The Role of Economic Plans”. ESRI Research Note No.27

https://www.esri.cao.go.jp/jp/esri/archive/e_rnote/e_rnote030/e_rnote027.pdf

Rei Sato (2023). “Japan’s Bubble-Burst: The Party That Wasn’t Supposed to End”. KonichiValue

https://www.konichivalue.com/p/japans-bubble-burst-the-party-that

World Bank (2006). “Japan – Moving Toward a More Advanced Knowledge Economy: Assessment and Lessons”. WBI Development Studies

https://documents.worldbank.org/en/publication/documents-reports/documentdetail/291071468040556431/assessment-and-lessons

DataQuest (1990). “Japanese Semiconductor Industry Service”. Computer History Museum

https://archive.computerhistory.org/resources/access/text/2013/04/102723222-05-01-acc.pdf

DataQuest (1986). “Japanese semiconductor industry service : seminar on improving international competitiveness”. Computer History Museum

https://www.computerhistory.org/collections/catalog/102723183

U.S. Congress, Office of Technology Assessment (1990). “The Big Picture: HDTV and High-Resolution Systems”. OTA-BP-CI’I’-64

https://digital.library.unt.edu/ark:/67531/metadc39964/

Doug O’Laughlin (2022). “Lessons from History: The 1990s Semiconductor Cycle(s)”. Fabricated Knowledge

https://www.fabricatedknowledge.com/p/lessons-from-history-the-1990s-semiconductor

John A. Mathews & Dong-Sung Cho (2009). “Tiger Technology: The Creation of a Semiconductor Industry in East Asia”. Cambridge University Press

https://doi.org/10.1017/CBO9780511552229

Yoshito Hirota (2021). “Transfer of Engineers from Japanese Electronics Companies to Samsung Based on Patent Information”. Journal of Economics (Japanese: “特許情報から見た技術者の「国際的」移動:日本企業からサムスンへ”・経済学雑誌)

https://dlisv03.media.osaka-cu.ac.jp/il/meta_pub/G0000438repository_24346063-121-2-1

Shun Sakuma (2022). “”Testimony of a Japanese Researcher Hired by Samsung in South Korea: A ‘Heavenly Environment’ with 1.7 Times the Salary”. Diamond Online (Japanese: “韓国サムスンに引き抜かれた日本人研究者の証言、給料1.7倍で「天国のような環境」”

https://diamond.jp/articles/-/308940

U.S. Congress, Office of Technology Assessment (1991). “Competing economies : America, Europe, and the Pacific Rim”. OTA-ITE-498, Chapter 7

https://www.econbiz.de/Record/competing-economies-america-europe-and-the-pacific-rim/10002111013

Toyota (2008). “A 75-year history through text”. Chapter 2, Sec. 2, Item 1

https://www.toyota-global.com/company/history_of_toyota/75years/text/leaping_forward_as_a_global_corporation/chapter2/section2/item1.html

Shiu-Wan Hung (2006). “Competitive strategies for Taiwan’s thin film transistor-liquid crystal display (TFT-LCD) industry”. Technology in Society

https://doi.org/10.1016/j.techsoc.2006.06.004

Jung, J. et al. (2023). “Recent progress in liquid crystal devices and materials of TFT-LCDs”. Journal of Information Display https://doi.org/10.1080/15980316.2023.2281224

Jang-Sup Shin (2015). “Dynamic Catch‐Up Strategy, Capability Expansion and Changing Windows of Opportunity in the Memory Industry”. GPN Working Paper No. 2015-001

https://doi.org/10.1016/j.respol.2016.09.009

Shin & Jang (2005). “Creating First-Mover Advantages: The Case of Samsung Electronics”. SCAPE

https://eaber.org/document/creating-first-mover-advantages-the-case-of-samsung-electronics/

Mathews (2005). “Strategy and the crystal cycle”. California Management Review, 47(2), 6–32

https://researchers.mq.edu.au/en/publications/strategy-and-the-crystal-cycle

U. Carmel (2017). “This is what a bubble looks like: Japan 1989 edition”. Investing.com

https://www.investing.com/analysis/this-is-what-a-bubble-looks-like:-japan-1989-edition-200197309

Nikkei Asia (2024). “On topic: What lies ahead for Japan after BOJ policy shift?”

https://asia.nikkei.com/Economy/Bank-of-Japan/On-topic-What-lies-ahead-for-Japan-after-BOJ-policy-shift

- Timing, location and harmony refers to the combination of both internal and external factors that helped Japan to recover quickly from war ruins. In terms of timing and location, Japan was among the beneficiaries of the US allies from the Korean War in 1950, as procurement and repair orders sparked Japan’s first postwar boom (Ishimaru, 2007). Same with Vietnam War in 1965, there is substantial evidence that Honda, Sony, and Mitsubishi Heavy Industries earned tidy profits from the war in Vietnam (Havens 1987; Shiraishi 1990), and Japan earned around $1 billion per year as a result of the conflict between 1965 and 1972 (Schaller, 1997).

For harmony, the Japanese government played a pivotal role in shaping economic and industrial strategies, coordinating policies across the public sector, and providing key guidance and information to the private sector to foster the growth of domestic enterprises. (Yoshioka & Kawasaki, 2016)

↩︎ - The interventionist approach is seen as “artificial” because it manipulates the value of the yen against the dollar, not due to economic conditions or Japan’s internal policies but as a concession to reduce the U.S. trade deficit.

↩︎ - Since the economy of Japan is highly dependent on exports, the stronger yen can make Japanese exports more expensive and less competitive in foreign markets; thus causing Japan to fall into a recession. Further perspectives from TMC (Toyota Motor Cooperation) showed that rapidly appreciating yen forced Japanese automakers to raise the prices of the exporting cars, and TMC suffered a huge drop in export volumes by 5.3% with decreasing operating income by 34.9 percent in 1986. (https://www.toyota-global.com/company/history_of_toyota/75years/text/leaping_forward_as_a_global_corporation/chapter2/section2/item1.html)

↩︎ - Normally, reverse brain drain happens when professionals studying and working abroad move back to their home country to contribute to the country’s development. However, the “reverse” brain drain in this article refers to a different situation: where human capital from a more developed country (Japan) migrates to a less developed country (e.g. Korea, Taiwan) to pursue better job opportunities and working environment.

↩︎ - Chaebols are large, family-owned business conglomerates in South Korea characterized by numerous subsidiaries across various industries. Despite their contribution to the country’s economic growth, chaebols have also faced criticism for issues such as monopolistic practices, lack of transparency, and political influence.

↩︎ - A 200mm wafer refers to a silicon wafer used in the fabrication of integrated circuits (ICs), microchips and other microelectronic devices

↩︎ - The book’s name in Japanese is “サムスンで働いてわかった 韓国エリートの仕事術” (2013) by Mizuta Takahisa.

↩︎ - In the 1990s, the world was focused on developing TFT-LCD technology for several key reasons: (1) thinner, lighter, better image quality and energy-efficient than traditional CRT displays; (2) boom in portable consumer electronics and industrial applications. ↩︎

This paper was written for an Economics course on Japanese economy (Social Issues in Contemporary Japan)