Written by Kha Nguyen

Edited by Genki Hase, Shan Min Kha & Jia Xuan Chok

On July 9, 2007, Chuck Prince, the former CEO of Citigroup, made a notorious comment:

“When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We’re still dancing.”

Just 14 months later, Lehman Brothers declared bankruptcy due to its losses on subprime mortgages, catalyzing a meltdown in the global financial system. The collapse of the mortgage market forced millions of Americans to lose their homes. US taxpayers had to bail out Citigroup with more than $470 billion in loans and guarantees—almost $4,000 per U.S. household.

***

The early 2000s were the time of turbulence for the US, characterized by the dot-com recession, the 9/11 terrorist attack, and wars in Iraq and Afghanistan. Domestic confidence plummeted; the US economy was stalling. To recover the economy, the US Federal Reserve System (FED) had no choice but to lower the interest rate to 1% to save the economy.

Since then, the “magma” of the asset price bubble started to boil alongside frantic capital lending ethics on Wall Street, all creating a huge financial “black-hole” beyond all control.

Real estate market

In short, the 2008 financial crisis was rooted in the real estate market—the hidden ticking time bomb waiting to explode.

In the early 1990s, the United States entered the decade with an eight-month mild recession, triggered by the Gulf War oil price shock and the cyclical business downturn since 1983. In response to rising unemployment, the FED decided to slash the federal funds rate from 8.25% in 1990 to 3% by 1993. This reduction in interest rates had a spillover effect throughout the economy, driving down long-term interest and mortgage rates.

After a mild recession, the US economy rebounded in 1993. From 1993 to 2000, the U.S. economy witnessed the strongest performance of the past three decades, characterized by low unemployment, robust economic growth, and minimal inflation. In the late 1990s, this economic prosperity resulted in a substantial acceleration in annual household incomes in the US, aligning with the entry of both baby boomers and Generation X into the workforce around the age of 20-30.

Driven by lower mortgage rates, higher earning potential, and the keen desire for homeownership, demand for housing skyrocketed at the end of the century. Between 1990 and 2000, approximately 17 million households of baby boomers and Gen X became homeowners, and over 16 million housing units were constructed to accommodate this increased demand.

Technology innovation and digitalization have played a critical role in laying the foundation for this economic boom. During the mid-1990s, the widespread adoption of personal computers and the expansion of the World Wide Web transformed various industries, including manufacturing, trade, finance and services. Starting in October 1998, waves of dot-com firms supported by venture capitalists went for initial public offerings (IPOs) regardless of the feasibility of their online business models. Although most of the internet start-ups hadn’t generated any revenue or profit yet, investors were drawn by the promise of future profitability. Nasdaq, the US technology index, rose by 800% in 1995-2000, from under 1.000 to a dizzying peak of 5048.62.

Ultimately, the dot-com bubble exploded. By the end of 2001, numerous dot-com stocks such as pets.com, Webvan, etoys, Kozmo, as well as prominent communication firms like Worldcom, NorthPoint Communications, and Global Crossing, crumbled and ceased operations. The stock market lost $5 trillion in market capitalization from its peak by the end of 2002.

In the aftermath of the dot-com bubble burst, investors flocked into the real estate market to safeguard their investments. A survey of homebuyers conducted in 2003 by Professor Robert Shiller at Yale University, discovered that ten times as many respondents were encouraged to buy a home due to the stock market collapse compared to those discouraged by it. Although the US real estate market experienced consistent growth in the late 1990s, this gradual rise escalated into overheating during the early 2000s until it peaked in 2006. (Graph 1)

Source: Barry Ritholtz (2009). “Case-Shiller: 2008 Home Prices Hit Record Declines”

Yet, the underlying cause for the 2008 financial crisis wasn’t solely the intensifying demand of the housing market but rather the consequences of an unregulated and overly bullish credit market.

Mortgage market

Before 2000, subprime mortgages were virtually non-existent. However, as property prices continued to climb and the increasing value of borrowers’ homes could always cover loan repayments, lenders found little justification for rejecting mortgage applicants with poor credit history (subprime loans), lacking verifiable income (Alt-A loans) and home equity as collateral. In 2006, the subprime mortgage business peaked when half of the mortgage market was captured by subprime, Alt-A and Home Equity Loan (HEL).

While subprime mortgages typically carry higher interest rates, the upward trajectory of housing prices has provided borrowers with the opportunity to “restructure” their mortgage loans. For instance, a 100% loan-to-value mortgage with no initial equity could see its loan-to-value ratio decrease to 80% as housing prices rise by 10-20% annually, transforming itself from “subprime” to “standard” mortgages with more favorable interest rates.

As the boom progressed, the shift into riskier lending became apparent in 2004. In 2005, mortgage origination for homebuyers coming from non-traditional amortization schedules (interest-only and negative amortization), made up nearly 30% of the entire home mortgage loans market, rising from just 1% in 2001 (Graph 2).

Retrieved from M. Baily (2008). “The Origins of the Financial Crisis”, Brookings

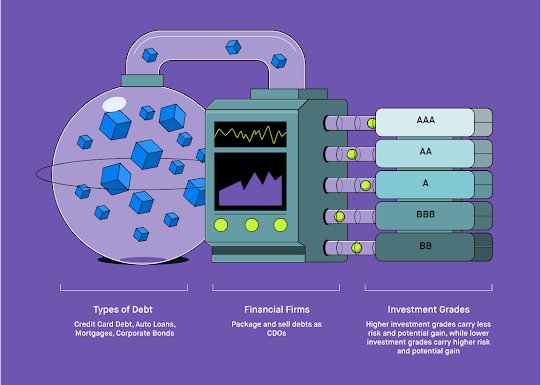

However, the proliferation of riskier subprime lending wasn’t simply facilitated by innovations in mortgage design. It was the concept of mortgage-backed securities (MBS) that truly unlocked the credit from the capital market.

Similar to the government issuing bonds with the promise of repayment backed by state finances, MBS also functions as a bond that is guaranteed by cash flow receivables from a mortgage borrower (those who borrowed money to buy a house) or a collection of mortgage loans.

Simply put, banks lend mortgages, then bundle them into MBS to diversify risk and sell them to investors for capital mobilization. Investors earn interest, while banks gain liquidity to provide more mortgage loans. If the borrowers default, banks confiscate the mortgaged property, and investors will be compensated by the sale of that property.

Source: Vancouver EC (2021)

By 2006, the subprime and Alt-A MBS issuing market was led by several ill-starred names such as Lehman Brothers, Bear Stearns, Countrywide, Washington Mutual, and Merrill Lynch. Among them, Fannie Mae and Freddie Mac were the pioneers in this game.

Fannie & Freddie, the two largest government-sponsored enterprises (GSEs) in the United States, were established to enhance access to affordable mortgage financing for individuals. Besides providing liquidity for the mortgage market through mortgage loans purchased from banks, Fannie & Freddie have also been involved in securitizing the mortgages they bought into MBS for sale in the open market.

In the efforts to meet the affordable housing goals pressured by the US Congress, the GSEs decided to issue their bonds and subsequently utilize the revenue to buy the MBS issued by private firms, injecting their funds into the market. Under the implicit federal government backing, Fannie & Freddie were able to pay a few points above Treasury yields on their bond issuance. With a lower cost of borrowing, the GSEs managed to yield enormous profits as they earned higher interest returns on MBS than they would pay on the bonds that they had issued.

From 2002-2007, Frannie & Freddie bought between $340 and $660 billion in private-label subprime and Alt-A MBS. From a market regulator, the GSEs have structurally become the facilitators fueling the US housing bubble.

Amidst the escalating housing prices, everything went smoothly: borrowers accessed mortgage loans for home purchases at low interest rates, banks received regular interest payments, and investors like GSEs enjoyed stable investment returns.

Yet, when the bubble bursts and house prices fall dramatically relative to the amount of mortgage debt outstanding, default rates for mortgage loans would skyrocket as the amount of unpaid principal balance on borrowers’ mortgages exceeds the market value of that home . This systematic mortgage crisis burst into flames in 2008, beginning with waves of default in subprime mortgages when these low-credit-score borrowers were granted hundreds of thousands of dollars to buy their expensive houses and cars. In fact, housing prices had plummeted so hard that even prime mortgages were defaulting as well.

Defaults in mortgage loans resulted in a detrimental spillover effect: investors fled the housing security market, banks incurred huge losses and debt, and the turmoil internalized into other financial sectors as banks lacked the liquidity to circulate capital. In the end, the credit market then came to a halt until the arrival of government interventions.

By 2008, Fannie & Freddie had held and guaranteed $5.4 trillion in mortgage debt assets and MBS. With the collapse of the housing market, these two mortgage giants combined had lost nearly $5.5 billion in the first two quarters of 2008. In September 2008, the Bush administration took their step to nationalize Fannie & Freddie to prevent their impending bankruptcy, thus shielding the US housing and financial market from further free-falling.

But all of this, from subprime mortgage lending to mortgage-backed securities (MBS), wasn’t enough for Wall Street bankers.

Collateralized Debt Obligations (CDOs) are another innovation of debt instruments that defined the further step in the world of securitization after 2000. With a similar structure as MBS, CDOs essentially “re-securitized” existing securities by bundling MBS and various asset-backed securities (ABS) that consisted of credit card, auto, corporate or student loans together. Under complex financial techniques of packaging different types of securities-debts with different risk exposures, CDOs can re-distribute risk extensively.

Retrieved from Robinhood Learn (2020)

This seemingly high-return, “risk-averse” business had pulled major players like Goldman Sachs, Mizuho, J.P. Morgan, and Credit Suisse to enter the CDO market, prompting them to issue their CDOs to raise more funds for their mortgage investment. Among these were Hudson Mezzanine Funding 2006-1 and Abacus 2007-AC1 of Goldman Sachs, Delphinus 2007-1 of Mizuho International, and Squared CDO 2007-1 of J.P. Morgan. The number of CDOs issued globally reached $500 billion in 2006, of which the ABS-based CDOs accounted for more than $300 billion (Graph 3)

Source: Reserve Bank of Australia (2007)

Miraculously, it is feasible to transform junk-rated CDOs into high-value assets. Through a combination of subprime MBS blending with other ABS and strategic purchases of credit default swaps (CDS), a low-range CDO can convert to medium-rated status. This credit manipulation explains why, despite historical data indicating high default rates for Baa-rated securities (the lowest investment grade above junk), those CDOs built of Baa2-rated MBS from Goldman Sachs and Mizuho were sold out for nearly $40 million in 2006-2007.

Along with the housing market crash, the quality of CDOs started to decline in 2007 because most of them were backed by home mortgages. In 2007, over 1,600 Moody-rated CDOs were downgraded, and many medium-rated and even top-rated securities also defaulted during this period. The securitization of subprime CDOs has severely destroyed the credit foundation in the financial market, eroding investors’ confidence in global credit rating systems, and amplifying the financial market crash in 2008. (Graph 4)

Source: Efraim Benmelech, 2010. “The Credit Rating Crisis”. National Bureau of Economic Research (NBER)

Leverage

Here are several outrageous figures that illustrate the extreme levels of leverage by banks before the 2008 crisis:

- Fannie & Freddie: 75 to 1 – including loans they owned and guaranteed as assets

- Bear Stearns: 35.6 to 1 – with only $11.1 billion of net equity supporting $395 billion in the company’s assets

- Lehman Brothers: 30.7 to 1; maintaining a hefty $690 billion in assets with just $22.5 billion in stockholders’ equity.

- Goldman Sachs: 22 to 1; with less than $5 in equity for every $100 borrowed

To achieve such colossal leverage without violating capital requirements, banks resorted to setting up ‘backyard’ companies known as Structured Investment Vehicles (SIVs).

SIVs are investment companies that borrow money by issuing short-term securities such as asset-backed commercial paper (ABCP) at low rates and then lend that money by buying MBS, CDOs and other higher-yield long-term securities. Since SIVs are bankruptcy-remote off-balance sheet entities, they could access lower interest rate funding through ABCP and borrow as much money as possible without the scrutiny of the capital requirement regulations.

These SIVs were major buyers of mortgage-backed securities (MBS), and their highly leveraged purchases injected an excessive amount of money into the housing market. This contributed significantly to rapidly rising asset prices, making them extremely vulnerable to the point where a decline in house prices could trigger waves of home mortgage loan defaults .

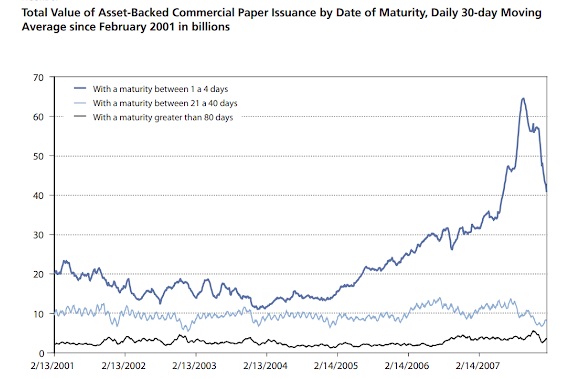

Until mid-2007, global SIV assets had reached $400 billion, according to Moody Ratings.

The leveraging rate in short-term borrowing became increasingly alarming in early 2006. Among the ABCP loans, papers with extremely short-term maturity (1-4 days) have skyrocketed drastically, from $20 billion in 2006 to $65 billion in 2008 (Figure 1). As short-term funding from ABCP began to dwindle in 2008 and investors declined to extend the debt maturity, many banks were exposed publicly with their minimal available capital in a “naked” position.

It turned out the leveraging game wasn’t confined to the US; it spread globally across Europe and beyond.

Take, for instance, IKB Deutsche Industriebank, a German bank specializing in financing medium-sized enterprises. Attracted by the invention of SIV, this bank had established Rhineland Funding Capital Corp. to delve into the US subprime mortgage securitization market, with the capital mobilized through ABCP from various American institutional investors, including the Montana Board of Investments, the city of Oakland, California, and the Robbinsdale Area School District in suburban Minneapolis. In July 2007, IKB stood at the brink of bankruptcy amid the subprime mortgage crisis, only to be rescued by an 8 billion euro bailout package from the German government-owned bank, KfW.

Macroeconomics

Before 2004, low interest rate policies had incentivized banks to borrow capital, allowing banks to utilize financial leverage for short-term borrowing (ABCP) and long-term investment (MBS, CDOs) to make profits from interest rate spreads. Starting in 2004, the FED began to raise interest rates above 5% in response to growing inflation concerns in the housing markets.

Theoretically, the rising FED funds rate should lead to an increasing long-term interest rate as well. However, as banks persisted in raising capital in the short-term and lending long-term, this has accidentally curbed the rise of long-term interest rates, including the long-term fixed mortgage rate. As long as the mortgage interest rate remained affordable, more and more people continued to take out home loans amid the inflating housing market.

In terms of externalities, since the early 2000s, trade liberalization has facilitated China’s rapid economic growth with the substantial accumulation of foreign reserves through export-oriented strategies. Similar to their neighbor, Southeast Asian nations had also sought to build up reserves to shield themselves from financial tsunamis since the 1997 Asian Financial Crisis. Japan, recovering from its own financial shock and housing bubble, began to look abroad for investment opportunities amid domestic stagnation.

As a result, these emerging Asian powerhouses have poured hundreds of billions of dollars of trade surpluses into the US. By 2008, net capital inflows into the US exceeded $1 trillion, with nearly half originating from China.

Retrieved from Paul Ramskogler (2015)

The capital inflow from Asian countries didn’t go straight into the securitized bond market; rather, it mostly went into US long-term government bonds. These international investment flows had kept the US long-term interest rates low, causing a crowding-out effect as investors turned to the securitized bond market (MBS, CDOs) in search of higher yields.

Retrieved from Paul Ramskogler (2015)

Instead of investing in manufacturing industries to enhance technology innovation, investors in the US were sneaking into Wall Street and its high-risk, high-return securitized bond market guaranteed by overpriced real estate. The bubbling lava of the housing market began to boil silently, and its collapse was just a matter of time.

Looking back, the 2008 financial crisis was driven by a series of factors: low interest rates, lenient mortgage lending practices, fraudulent activities, and the desire for homeownership. Michael Lewis, an American financial journalist in “The Big Short,” pointed out that the crisis wasn’t purely caused by subprime loans in 2005 but also by the long-standing concept of securitization, nurtured by major banks since 1985. But once again, the issue lies not within the financial instruments themselves but rather in their misuse by profit-driven bankers and opportunistic venture capitalists.

Risks can be reduced by diversification. Yet, when issuing millions of dollars in MBS or CDOs filled with “diversified” mortgages, those risks would be dispersed in unknown directions. Nobody realized who was responsible for the initial paycheck underneath the “pool” of guaranteed assets, and no one knew where to fix when it “leaked”.

References:

Adam Hayes, 2022. “Structured Investment Vehicle: Overview, History, Examples”, Investopedia https://www.investopedia.com/terms/s/structured-investment-vehicle.asp

Backman, Lowery & Pentis, 2024. “Historical mortgage rates: A look at home loan trends over time”, CNN https://edition.cnn.com/cnn-underscored/money/historical-mortgage-rates

Bank of America, 2008. “SIVs – Past, Present and Future”. https://www.cacttc.org/assets/documents/JP%20Borella%20-%20SIVs.pdf

Barry Ritholtz, 2009. “Case-Shiller: 2008 Home Prices Hit Record Declines” https://ritholtz.com/2009/02/case-shiller-2008-home-prices-hit-record-lows/

Barry Ritholtz, 2010. “CDOs for Dummies”. https://ritholtz.com/2010/05/cdos-for-dummies/

Brian McCullough, 2018. “A revealing look at the dot-com bubble of 2000”. TED Ideas https://ideas.ted.com/an-eye-opening-look-at-the-dot-com-bubble-of-2000-and-how-it-shapes-our-lives-today

Chris Alden, 2005. “Looking back on the crash”, The Guardian https://www.theguardian.com/technology/2005/mar/10/newmedia.media

Daniel Covitz, Nellie Liang & Gustavo Suarez, 2009. “The Evolution of a Financial Crisis”, The Federal Reserve Board. https://www.federalreserve.gov/pubs/feds/2009/200936/index.html

Edward S. Steffelin, 2011. “J.P.Morgan Securities LLC”, US Securities and Exchange Commission https://www.sec.gov/litigation/litreleases/lr-22008

Efraim Benmelech, 2010. “The Credit Rating Crisis”. US National Bureau of Economic Research (NBER) https://www.nber.org/reporter/2010number1/credit-rating-crisis

Goldman Sachs, 2019. “The Late 1990s Dot-Com Bubble Implodes in 2000” https://www.goldmansachs.com/our-firm/history/moments/2000-dot-com-bubble.html

Greg Ip, “The Worst Ideas of the Decade: Housing Prices Always Rise”, Washington Post https://www.washingtonpost.com/wp-srv/special/opinions/outlook/worst-ideas/housing-bubble.html

J. Griffith, 2012. “The $5 Trillion Question: What Should We Do with Fannie & Freddie?”, American Progress https://www.americanprogress.org/article/the-5-trillion-question-what-should-we-do-with-fannie-&-freddie

Janet Tavakoli, 2010. “Goldman Sachs: Spinning Gold”, Tavakoli Structured Finance LLC https://www.tavakolistructuredfinance.com/2010/04/goldman-sachs-bailout/

Jason Thomas, 2010. “Housing Policy, Subprime Markets and Fannie Mae & Freddie Mac”. St. Louis FED Conference. https://files.stlouisfed.org/files/htdocs/conferences/gse/Van_Order.pdf

Jason Thomas, 2013. “Fannie, Freddie, and the Crisis”, National Affairs https://www.nationalaffairs.com/publications/detail/fannie-freddie-and-the-crisis

John Lovito & Charles Tan, 2023. “What Are Treasury Yields Telling Us About the Market Climate?”. American Century Investments https://www.americancentury.com/insights/what-are-treasury-yields-telling-us-about-the-market-climate/

Joint Center for Housing Studies of Harvard University (JCHS), 2004. “The state of the nation’s housing 2004” https://www.jchs.harvard.edu/research-areas/reports/state-nations-housing-2004

Jonathan Lansner, 2022. “1987: When mortgage rates last soared this much”. The Orange County Register https://www.ocregister.com/2022/06/18/1987-when-mortgage-rates-last-soared-this-much/

Ksenia Potapov, 2023. “1990s Nostalgia Hits the Housing Market, With One Key Difference”, First American https://blog.firstam.com/economics/1990s-nostalgia-hits-the-housing-market-with-one-key-difference

M. Baily, M. Johnson & R. Litan, 2008. “The Origins of the Financial Crisis”, Brookings https://www.brookings.edu/articles/the-origins-of-the-financial-crisis/

Paul Ramskogler, 2015. “Tracing the origins of the financial crisis”, OECD Journal https://doi.org/10.1787/fmt-2014-5js3dqmsl4br

R. Wiggins & A. Metrick, 2019. “The Lehman Brothers Bankruptcy”, Journal of Financial Crisis https://elischolar.library.yale.edu/journal-of-financial-crises/vol1/iss1/4/

Reserve Bank of Australia, 2007. “Recent Developments in Collateralized Debt Obligations in Australia” https://www.rba.gov.au/publications/bulletin/2007/nov/1.html

Richard Tomlinson & David Evans, 2007. “A ratings charade”, The Seattle Times https://www.seattletimes.com/business/a-ratings-charade/

Robinhood Learn, 2020. “What is a Collateralized Debt Obligation (CDO)?” https://learn.robinhood.com/articles/7yHAH6m6oPWEOyjIjZtSZ9/what-is-a-collateralized-debt-obligation-cdo/

Roddy Boyd, 2008. “The last days of Bear Stearns”. CNN Money https://web.archive.org/web/https://money.cnn.com/2008/03/28/magazines/fortune/boyd_bear.fortune/

Roger L. Martin and Alison Kemper, 2015. “The Overvaluation Trap”, Harvard Business Review https://hbr.org/2015/12/the-overvaluation-trap

The Financial Crisis Inquiry Commission, 2011. “The Financial Crisis Inquiry Report” https://www.govinfo.gov/app/details/GPO-FCIC

Vancouver Economic Commission, 2021. “Another Entrant for Financing Decarbonized Buildings” https://vancouvereconomic.com/blog/news/another-entrant-for-financing-decarbonized-buildings-sustainable

Vintti, 2023. “Structured Investment Vehicles (SIV): Finance Explained” https://vintti.com/blog/structured-investment-vehicles-siv-finance-explained/

W. Edelberg & N. Steinmetz-Silber, 2023. “High mortgage rates are probably here for a while”, Brookings https://www.brookings.edu/articles/high-mortgage-rates-are-probably-here-for-a-while/